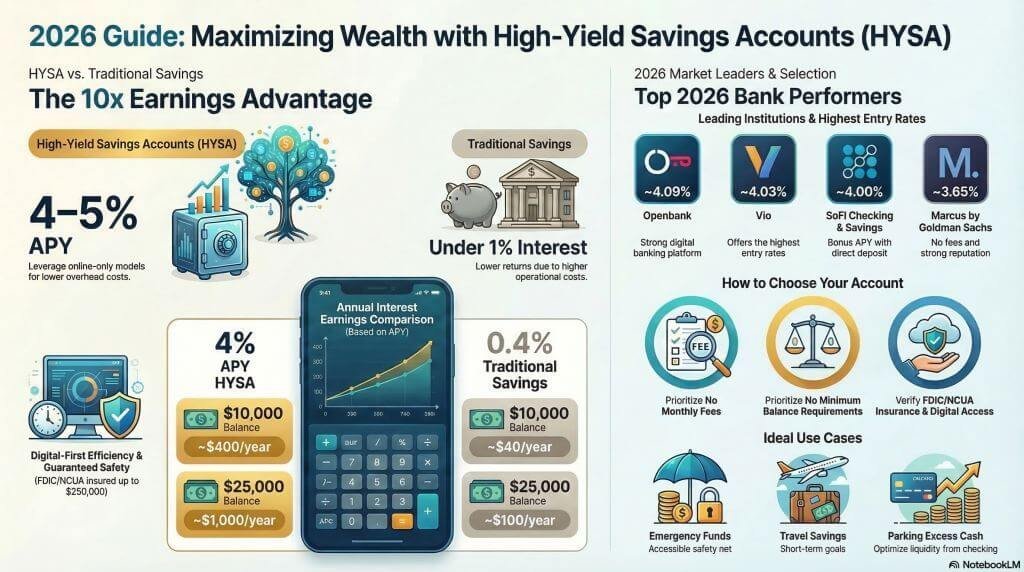

One of the easiest ways to build your savings at a high rate of interest while also keeping your money safe and accessible to you quickly is through a high-yield savings account (HYSA). Most online banks and financial technology (fintech) companies have offered annual percentage yield (APY) rates varying between approximately 4% and 5% in 2026.

These rates are far greater than those available in a traditional savings account; however, for comparison’s sake, the average interest rate on a savings account at banks in the U.S. during the past year has been substantially less than one percent (1%).

Additionally, several of the best HYSA institutions will offer significantly greater interest earnings than traditional savings accounts at the same time on the same balance.

In this guide, we will summarise all the best HYSA’s available in 2026, as well as each account’s APY, features, and eligibility requirements, so that you will have an idea of which high-yield savings account might be best suited to help you achieve your overall financial objectives.

Table of Contents

What Is a High-Yield Savings Account?

High-yield savings accounts are a type of savings account through banks and credit unions that provide customers with larger rates of interest (i.e., higher Annual Percentage Rates, or APYs) than standard savings accounts.

Primary Features

1. Large APY compared to traditional savers

2. Simple online access through app or web banking (no paper checks)

3. FDIC/NCA insured to $250,000 per depositor for catastrophic loss

4. Many HYSAs have no or very few monthly maintenance fees, and

5. Easy access to deposits and withdrawals with no/little limitation

For emergency savings accounts and short-term savings, your safety and liquidity, plus your return on investment, make HYSAs a great way to reach your savings goals.

How Much Interest Can You Earn?

A traditional savings account has significantly different interest rates than a high-yield savings account.

| Balance | 4% APY HYSA | 0.4% Traditional Savings |

| $5,000 | ~$200/year | ~$20/year |

| $10,000 | ~$400/year | ~$40/year |

| $25,000 | ~$1,000/year | ~$100/year |

If you were to put $10,000 in either type of savings account earning 4% APY per year, you would not receive $400 from a low-rate account; instead, you’d only receive around $40.

What Is the Best High-Yield Savings Account in 2026?

Typically, high-yield savings accounts provide the following 3 features:

- Interest Rates between 4% and 5%

- Monthly Maintenance Fees That Are Not Charged

- No Minimum Balance

An example of some of the best high-yield savings accounts to consider for 2026 includes;

- Varo

- Openbank

- Vio Online Banking

- SoFi

- Marcus Goldman Sachs

Currently, some of the leading savings accounts are paying APYs between 4% and 5%, based on the requirements for opening the account, such as direct deposit.

Best High-Yield Savings Accounts List

The following compares how several of the top competitors in the U.S. marketplace provide their savings accounts.

| Bank / Institution | APY (Approx.) | Minimum Deposit | Key Features |

| SoFi Checking & Savings | Up to ~4.00% | $0 | Bonus APY with direct deposit |

| Openbank High-Yield Savings | ~4.09% | $500 | Strong digital banking platform |

| Vio Bank Savings | ~4.03% | $100 | Competitive APY with low entry |

| Marcus by Goldman Sachs | ~3.65% | $0 | No fees and a strong reputation |

| American Express High Yield Savings | ~3.30% | $0 | Trusted brand and easy transfers |

Interest rates can fluctuate based on the current Federal Reserve monetary policy or other factors impacting the financial industry.

While some financial institutions may provide an added incentive to use their account via a promotional APY or special interest rate for a certain length of time, there are often stipulations that must be met before receiving such benefits; these stipulations typically include requirements for automatic deposits and/or monthly debit transactions.

Quick Comparison: HYSA vs Traditional Savings

| Feature | High-Yield Savings | Traditional Savings |

| Typical APY | ~4%–5% | ~0.01%–0.6% |

| Fees Usually none | Sometimes | monthly |

| Accessibility | Mostly online | Branch banking |

| FDIC Insurance | Yes | Yes |

| Best Use | Emergency fund or short-term savings | Basic banking |

The disparity in annual percentage yield between an HYSA and a conventional savings account can result in significantly higher interest accumulation on the account over extended periods.

For instance, take the following examples:

- A $10,000 deposit earning four per cent (4%) will earn about $400 interest annually.

- A $10,000 deposit earning four per cent (0.4%) will earn about $40 interest annually.

Why are HYSAs different?

HYSAs differ primarily from traditional savings accounts in terms of their annual percentage yield (APY), i.e., the amount of interest the customer’s deposit earns. Most HYSAs are offered only through internet banking, so they do not have many physical branches where customers can make deposits or withdrawals, which saves banks the time and expense of training bank employees.

How to Choose the Best HYSA

When evaluating high-yield savings accounts, it’s critical to understand what factors will affect your overall return, including but not limited to APY.

1. Annual Percentage Yield (APY)

APY (Annual Percentage Yield) is a measure of how much interest your account will yield annually.

For rates comparable to today’s values of 4% or higher APY in 2026, you’ll need to search for competitive rates.

2. Fees and Minimum Balance

Fees can take away from your interest earnings over time.

Choose accounts with:

- No monthly maintenance fees.

- No minimum balance requirements.

3. Accessibility and Transfers

Consider how quickly you can access your funds. If you plan to do so using a mobile banking application, online banking, external bank transfers, or an ATM/debit card, be sure to verify these options before opening an account.

4. Deposit Insurance

Make certain that your account will be insured by the FDIC (for banks) or the NCUA (for credit unions), so you’ll be covered for deposits up to $250,000 per account holder.

Choosing where to keep your hard-earned money can get confusing; however, by knowing which terms are most important to focus on, it should help clarify your decision about where to open a new account or put money away into savings.

Why HYSAs Are Popular in 2026

HYSAs have gained attention for a variety of reasons.

Higher interest rates

4-5% APY is far above what most banks are offering for savings accounts.

Inflation protection

Adequate options for inflation protection

The better yield on HYSAs ensures that your savings can provide you with increased gains over time and will maintain its purchasing power.

Low-risk financial product

HYSAs are to be viewed as very stable investments compared with other forms of investing, including stocks and cryptocurrencies. HYSAs provide an individual with:

- Very stable returns

- Maintaining capital

- Easy access to cash

Pros and Cons of HYSA

The Advantages & Disadvantages of a High-Yield Savings Account:

Advantages

- Greater Amount of Interest Earned

- Insured & Secure Deposits

- Easy Online Management

- No Locking Period Like CDs

Disadvantages

- Interest Rates Are Variable

- Best APY May Require Direct Deposits

- No Physical Branches Available

Nonetheless, HYSAs Continue To Be Amongst The Class Of Low-Risk Storing Options For Your Funds.

Best Use Cases for High-Yield Savings Accounts

High-yield savings accounts can be an effective tool for many or various/other purposes (financial goals: money,etc).

Examples of the best uses for high-yield savings accounts include:

Emergency Funds: You can keep funds needed to cover emergencies in a high-yield savings account, while earning interest.

Short-term Savings Goals: Travel funds, down payments, and expenses related to the holidays are three examples of short-term savings goals.

Cash Management: Many people choose to use high-yield savings accounts to “park” extra cash, rather than leaving those dollars sitting in their checking account(s).

Final Thoughts

In 2026, the top high-yield savings accounts provide not only great opportunities to increase your money without sacrificing safety, but also offer potentially significant degrees of flexibility for continued access to funds.

By transferring deposits from checking accounts to high-yield savings accounts (HYSA) with many online banking establishments, depositors can earn interest on their deposits at rates greater than 4%.

When evaluating different types of accounts, it is important for depositors to evaluate the annual percentage yield (APY), the costs associated with maintaining the account, the minimum amount needed in the account to keep it open, and the level of access available. Evaluating these items will help you select the best option based on your financial circumstances, which may be the establishment of an emergency fund or the maximisation of returns on excess cash.

Frequently Asked Questions

What is the highest-paying HYSA in 2026?

Banks may advertise an APY of almost 5%, depending on promotional offers, requirements such as direct deposits, and balance thresholds.

Are high-yield savings accounts safe?

There is no risk associated with a high-yield savings account. Savings accounts at banks and credit unions are insured by the FDIC or NCUA for up to $250,000 per customer.

Can you withdraw money anytime from a HYSA?

You may withdraw or transfer money from your high-yield savings account at any time; however, some banks will limit the number of withdrawals or transfers you can make each month.

Do high-yield savings rates change?

Yes. High-yield savings account rates are variable and can change each month in relation to changes in the federal funds rate and overall economic factors.